The Trump 2.0 Era: What Kind of Government Can We Expect, and How Will It Impact Markets?

Donald Trump has officially become the 47th President of the United States.

The new administration is expected to act swiftly, leveraging executive orders (comparable to legislative decrees in other systems), which take immediate effect and bypass the traditional legislative process, including Congressional approval.

"I will act with historic speed and strength and fix every single crisis facing our country," declared the newly elected President.

|

| Evan Vucci/AP |

Key Priorities of the Trump Administration

Immigration Reduction:

Expected to lead to immediate wage pressures as companies struggle to find lower-cost labor, potentially driving inflation higher.

A similar market dynamic was observed in the UK post-Brexit, where reduced immigration contributed to "stickier" inflation, with average inflation remaining higher compared to the EU since the start of the war. This forced the Bank of England to implement more aggressive measures to control price growth.

Tariff Increases:

While tariffs generally exert inflationary pressure on prices, their application may not be immediate or uniform. Trump has reiterated plans to impose a 25% tariff on imports from Mexico and Canada starting February 1.

China remains a primary target, with potential tariffs on 100% of its exported goods. Conversely, Europe might face different terms.

Deregulation Across Sectors:

Energy, technology, pharmaceuticals, and cryptocurrencies are among the sectors likely to experience regulatory easing.

Potential Trade Negotiations

Europe:

Trump aims to negotiate the removal of the digital tax impacting U.S. Big Tech companies and push for increased European imports of U.S. Liquefied Natural Gas (LNG).

Europe’s unanimous agreement on purchasing more U.S. LNG may face resistance from countries like Hungary and Slovakia, which rely heavily on Russian supplies. However, Trump's strong ties with Hungary's leadership could play a decisive role.

An increase in U.S. LNG imports would likely raise energy bills in Europe due to its higher cost compared to Russian gas.

Source: S&P Global Commodity Insights / Credit: CI Content Design

Canada and Mexico:

These two countries account for over a quarter of U.S. imports across various sectors, including agriculture, automotive, and industrial goods.

While Trump's tariff threats may serve primarily as a negotiation tactic, they could disrupt supply chains, raising production and consumer prices in the U.S.

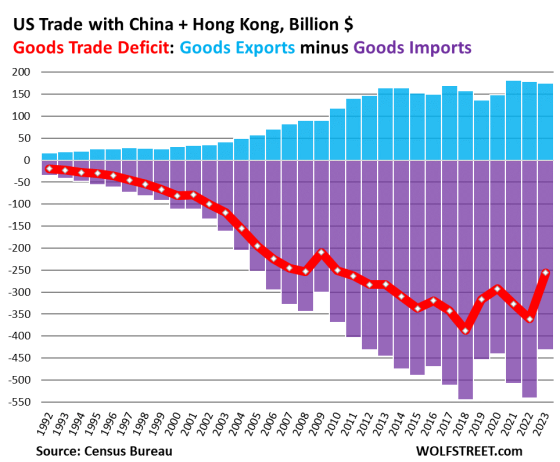

China:

Tariffs may reduce the U.S.-China trade deficit (previously trimmed from $400 billion to $250 billion during Trump's first term). However, such measures could harm U.S. industrial output, as seen in 2019 when manufacturing activity slowed significantly due to escalating trade tensions.

Negotiation Strategies:

Treasury Secretary Bessent is described as a "gradualist" regarding tariffs, favoring future guidance and conditional application based on negotiated agreements with trading partners. Germany and Vietnam were specifically mentioned as examples.

Trade Representative Lutnick advocates for imposing tariffs only on industries where the U.S. has competitive production, such as foreign automotive imports. This approach seeks to minimize inflationary impact and maximize strategic gains.

A Glance Back: Trump’s First Term Economic Impact

During Trump’s initial term, the U.S. economy experienced both notable achievements and challenges:

Economic Growth:

Corporate tax cuts (from 35% to 21%) boosted GDP growth to over 3% and spurred stock market gains. The S&P 500 delivered an average quarterly return of +4.5% in 2017.

Volatility and Trade Wars:

Tariff policies introduced in 2018 led to market volatility (-1% quarterly average return for the S&P 500 that year) and slower GDP growth (averaging 2%).

Retaliatory measures from Europe included tariffs on U.S. steel, aluminum, and agricultural products, among others.

Inflation and Employment:

Inflation rose to nearly 3% during Trump’s tenure, compared to 1.5% under Obama. However, the employment rate improved significantly, with workforce participation increasing from 59.7% pre-Trump to 61.1% by late 2019.

.png)

Challenges with China:

Ongoing tariffs led to retaliatory actions, such as China’s currency devaluation, which further strained U.S. industrial production and slowed economic growth in 2019.

.png)

Lessons from Past Tariff Strategies

In May 2019, during Trump’s first term, a 5% tariff on Mexican imports was announced, with plans to increase to 25% over subsequent months. However, these tariffs were suspended within a month following a favorable trade and immigration agreement with Mexico. This underscores Trump’s use of tariffs as a negotiation tool rather than a long-term economic strategy.

Similarly, the administration’s approach to tariffs under Bessent and Lutnick reflects a calculated strategy aimed at leveraging trade relationships without overburdening U.S. markets.

Market Outlook Under Trump 2.0

While Trump’s policies on fiscal reductions could provide a short-term boost to the U.S. economy, the long-term impact will hinge on global responses, particularly from Europe and China.

China, the third-largest trading partner for the U.S., remains critical. Although the trade deficit has improved, reliance on Chinese imports continues, leaving the U.S. economy vulnerable to potential shocks and heightened market volatility.

In summary, Trump’s approach—focused on aggressive negotiations and fiscal easing—may deliver immediate economic gains. However, the uncertainty surrounding retaliatory measures and global trade dynamics could pose significant risks to markets in the months ahead.

Comments

Post a Comment